What if your corporate structure could do more than just hold assets, acting instead as a secure bridge to the European market and a permanent shield for your global wealth? For many international investors, the prospect of setting up a holding company in Portugal is attractive yet clouded by technical uncertainty. You likely understand the strategic value of an EU base, but the choice between an SGPS and a standard Lda structure often creates unnecessary friction. It's common to feel concerned about navigating non-resident banking hurdles or meeting the evolving substance requirements mandated by the EU.

We're here to replace that confusion with a clear, actionable strategy. This guide explores how you can leverage Portugal's 100% participation exemption on dividends and capital gains to maximize your global returns. You'll discover a streamlined roadmap that connects company formation with residency visas and robust asset protection. We'll examine the 2026 tax environment, including the phased reduction of corporate tax rates to 17% by 2028, to ensure your structure is both compliant and highly efficient for the long term.

Key Takeaways

- Understand the modern shift from traditional SGPS entities to flexible Lda or SA structures when setting up a holding company in Portugal.

- Identify the specific criteria needed to qualify for the participation exemption, which provides 100% tax relief on dividends and capital gains.

- Evaluate the strategic benefits of the Madeira International Business Centre (MIBC) to access a competitive 5% corporate tax rate until 2033.

- Navigate the incorporation process with a clear roadmap, from securing a non-resident NIF to completing registration in approximately one to three weeks.

- Learn how to align your corporate holding structure with Portuguese residency programs to secure long term EU market access and global mobility.

What is a Portuguese Holding Company (SGPS) in 2026?

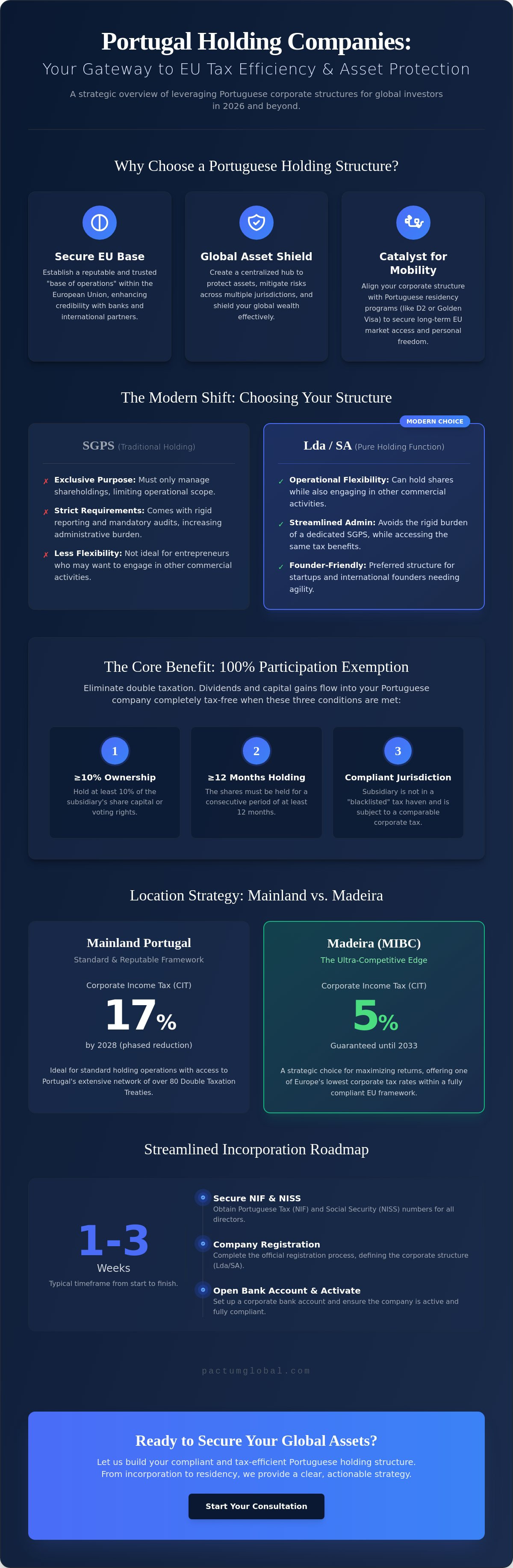

A Portuguese holding company is a corporate vehicle designed specifically to manage and consolidate shareholdings in other businesses. Traditionally, this is known as an SGPS (Sociedade Gestora de Participações Sociais). For decades, the SGPS was the default choice for investors. However, the regulatory landscape in 2026 has evolved. While the SGPS remains a valid legal structure, many international entrepreneurs now opt for standard limited liability companies, such as an Lda or SA, to perform "pure holding" functions. This shift offers greater operational flexibility while still accessing the same elite tax benefits.

The primary reason for setting up a holding company in Portugal is to create a centralized hub for asset protection and tax optimization. By using a Portuguese entity, you can mitigate risks across multiple jurisdictions and streamline your global cash flow. Portugal has solidified its position as a premier EU hub because it balances high-level legal security with a pro-business environment. It's no longer just about the tax rate; it's about having a reputable "base of operations" that banks and international partners trust. Understanding the variety of business entities in Portugal is the first step toward building this foundation.

The Legal Framework: SGPS vs. Pure Holding Functions

In 2026, the distinction between a formal SGPS and a standard Lda acting as a holding is critical. An SGPS must have the exclusive corporate purpose of managing shareholdings. This comes with strict reporting requirements and mandatory audits. Conversely, a standard Lda can hold shares while also engaging in other commercial activities. This flexibility is why many founders prefer the Lda structure. It allows you to manage your subsidiaries without the rigid administrative burden of a dedicated SGPS, provided you meet the substance requirements necessary for tax compliance.

Who Benefits Most from a Portuguese Structure?

International founders targeting EU expansion find Portugal an ideal gateway. It's particularly effective for investors managing assets across the Lusophone world, including Brazil and Angola, due to existing double taxation treaties. Startups also benefit significantly. If you're preparing for venture capital rounds, using a Portuguese holding structure helps organize your equity through SAFE or SHA contracts. Beyond the corporate benefits, setting up a holding company in Portugal often serves as a catalyst for global mobility. We frequently help clients integrate their corporate setup with residency applications, such as the D2 or Golden Visa, ensuring their business growth aligns with their personal freedom.

The Participation Exemption: Eliminating Double Taxation

Double taxation is often the greatest hurdle for international investors managing multiple subsidiaries. Without the right structure, your profits can be taxed once in the country of origin and again when they reach the parent company. When setting up a holding company in Portugal, you gain access to one of Europe's most robust participation exemption regimes. This legal framework is designed specifically to eliminate that redundancy. It allows dividends and capital gains to flow into your Portuguese entity with 100% tax relief, provided certain criteria are met. This efficiency is further bolstered by Portugal's network of over 80 Double Taxation Treaties (DTTs), which protect your global income from being eroded by competing tax jurisdictions.

The regime doesn't just apply to incoming dividends. It also covers the disposal of shares. If you decide to sell a subsidiary, the capital gains realized from that sale can be entirely exempt from Corporate Income Tax (CIT). This makes Portugal an exceptionally strong "exit" jurisdiction for founders and venture capital groups. By centralizing your holdings here, you create a tax-neutral environment that facilitates easier reinvestment and more efficient capital allocation across your global portfolio.

The 10-12-10 Rule: Key Requirements for Tax Exemption

To qualify for the 100% exemption on dividends and capital gains, your holding must meet three primary conditions. First, your Portuguese company must hold at least 10% of the share capital or voting rights of the subsidiary. Second, these shares must be held for a consecutive period of at least 12 months. Third, the subsidiary must be subject to a corporate tax rate that is at least 60% of the Portuguese CIT rate. It's also vital to ensure the subsidiary isn't located in a jurisdiction on Portugal's "blacklisted" tax haven list. Meeting these benchmarks ensures your income remains protected and fully compliant with EU standards.

Underlying Tax Credits and Group Taxation

What happens if your structure doesn't perfectly meet the participation exemption criteria? This is where many competitors stop, but the Portuguese system offers a safety net through the Underlying Tax Credit. If the exemption isn't available, you can often still credit the tax paid by the subsidiary abroad against your Portuguese tax liability. For larger operations, the Special Regime for Group Taxation (RETGS) allows you to consolidate profits and losses across your Portuguese entities, significantly reducing the overall tax burden. Properly drafting Shareholders Agreements (SHA) is essential during this phase to manage group-level distributions and protect the interests of all parties involved. If you're unsure how these group rules apply to your specific portfolio, the team at pactumglobal.com can help you map out a compliant path forward.

Location Strategy: Mainland Portugal vs. Madeira (MIBC)

Choosing the right physical location for your entity is a pivotal decision when setting up a holding company in Portugal. While the entire country operates under the same national legal framework, the fiscal reality varies significantly between the mainland and the Autonomous Region of Madeira. In 2026, the standard Corporate Income Tax (CIT) rate in mainland Portugal is 19%. This is already competitive within the European Union, especially with the government's phased plan to reduce this rate to 17% by 2028. However, for international investors with specific high-growth profiles, the Madeira International Business Centre (MIBC) offers a distinct alternative that often serves as the "gold standard" for holding structures.

The decision isn't purely about the headline tax rate. It's about balancing fiscal efficiency with the operational needs of your group. A mainland company in Lisbon or Porto provides immediate access to a vibrant tech ecosystem and a deep pool of local talent. Conversely, a Madeira-based company offers elite tax benefits but requires a more specific commitment to local substance. Your choice will define how your brand is perceived by international partners and how easily you can scale your operations across the EU.

The Madeira International Business Centre (MIBC) Advantage

The MIBC is a highly regulated, EU-approved preferential tax regime. It's not a "tax haven" but a sophisticated tool for economic development. Qualifying companies benefit from a 5% corporate tax rate on income derived from non-resident entities. This rate is guaranteed until December 31, 2033, provided the company is licensed by the end of 2026. The trade-off for this 5% rate is a clear requirement for substance. You must create a minimum number of jobs in the region or meet specific investment thresholds in local assets. These rules ensure the structure is robust enough to withstand international tax scrutiny while protecting your global profits.

Lisbon and Porto: The "Mainland" Holding Alternative

A standard mainland company is often more appropriate if your holding company will also act as an operational headquarters. If you need to hire a large team or integrate closely with the local market, Lisbon and Porto are unmatched. These cities are the heart of the Portuguese business world, offering world-class infrastructure and a prestigious corporate image. Using a mainland entity also simplifies the process if you're following our Portugal business setup guide to launch an active service or tech business. While the CIT is higher than in Madeira, the 15% reduced rate on the first €50,000 of taxable income for SMEs provides a helpful cushion for smaller holding structures. Ultimately, setting up a holding company in Portugal on the mainland prioritizes ecosystem access and talent over the absolute lowest tax percentage.

Roadmap to Incorporation: From NIF to Active Compliance

The actual process of setting up a holding company in Portugal is remarkably efficient once you have the foundational documents in place. In 2026, the timeline for formation typically spans one to three weeks. While digital-first initiatives like "Empresa na Hora" (Company on the Spot) allow for immediate incorporation using pre-approved templates, these aren't always ideal for complex holding structures. A strategic holding entity often requires customized Articles of Association to define specific governance, voting rights, and distribution rules that generic templates don't provide.

Before any registration occurs, every non-resident shareholder and director must obtain a Portuguese Tax Identification Number (NIF). This is the administrative key to the country. Following this, the 2026 banking landscape presents the most significant hurdle. Unlike simple registration, opening a business bank account requires navigating rigorous "Know Your Customer" (KYC) and Anti-Money Laundering (AML) protocols. Banks now demand detailed proof of the source of funds and the ultimate business purpose. We manage this complexity by preparing a comprehensive "bank-ready" file that anticipates these questions before they're asked, ensuring a smoother approval process.

Step-by-Step Incorporation Checklist

- Name Reservation: You must select and reserve a unique name with the National Registry of Collective Entities (RNPC) to avoid legal conflicts.

- Tailored Articles: We avoid generic templates. Your Articles of Association should clearly outline the holding's specific purpose and management powers.

- RCBE Registration: To comply with EU transparency laws, you must register the Ultimate Beneficial Owner (RCBE). This identifies who truly controls the company to the authorities.

Economic Substance and 2026 Compliance

The era of "letterbox companies" is over. Under current EU directives, a holding company must demonstrate "adequate substance" to benefit from the participation exemption and other tax treaties. This means the company can't exist merely on paper. It requires a physical presence, such as a dedicated office space, and evidence that key decisions are made within Portuguese territory. Substance is a shield against tax audits.

Substance is also demonstrated through management. Having local directors or a qualified team on the ground strengthens your claim that the "Place of Effective Management" is indeed Portugal. Beyond setup, your holding has ongoing obligations. This includes mandatory annual audits for larger entities and the filing of the annual corporate tax return (Modelo 22) every May. Ensuring these active compliance steps are met is what protects your assets from future regulatory challenges. If you're ready to begin the process with a partner who understands these nuances, explore our professional services for setting up a holding company in Portugal.

Securing Your Global Assets with Pactum Global

Setting up a holding company in Portugal is a strategic move that demands more than a simple filing. International founders often find that off-the-shelf solutions fail when they encounter complex cross-border needs. A generic setup might register your company, but it won't align your corporate governance with your long-term residency goals or your family’s inheritance plan. We bridge this gap by integrating legal authority with a supportive, clear process that treats your business as a whole.

The Brazil-Portugal Corridor represents a unique opportunity for South American investors. By centralizing assets in a Portuguese holding, you create a stable, Euro-denominated hub that optimizes Brazilian capital while mitigating currency volatility. This structure is vital for managing cross-border inheritance and protecting your family’s future. We help you draft custom succession documents that ensure your wealth is preserved across generations, regardless of where your heirs reside. It’s about building a legacy that’s as international as your business.

Integrating Global Mobility and Corporate Law

Your corporate structure is a powerful tool for personal freedom. When setting up a holding company in Portugal, the entity can directly support your Portugal D2 Visa requirements by demonstrating a genuine economic commitment to the country. This presence facilitates family reunification and provides a clear path to EU residency. We act as your Global Navigator, ensuring every corporate decision also serves your immigration strategy. We handle the bureaucracy so you can focus on leading your group's expansion with confidence.

Cross-Border Asset Protection: The Pactum Advantage

Protection extends beyond tax efficiency. By centralizing your Intellectual Property and Trademarks within your Portuguese entity, you secure your brand’s value across the European market. This is particularly effective for founders moving a business to the USA from Brazil through a European intermediary. A Portuguese hub provides a layer of legal separation and access to favorable tax treaties that a direct Brazil-US move often lacks. Our approach combines tailored Shareholders' Contracts (SHA) with robust asset protection to keep your global portfolio secure. Whether you're setting up a holding company in Portugal for the first time or restructuring an existing group, we provide the steady hand needed for international success.

Future-Proof Your Global Corporate Structure

A Portuguese holding company is no longer just a tax-efficient vehicle; it's a vital anchor for international entrepreneurs seeking stability in the EU. The process of setting up a holding company in Portugal provides a unique gateway to the European market while safeguarding your wealth through the 100% participation exemption. Whether you're consolidating assets through the Brazil-Portugal corridor or preparing for a US expansion, the right foundation ensures your growth is both compliant and scalable.

At Pactum Global, we provide the expert navigation required for these complex transitions. Our team specializes in the end-to-end management of corporate setups and immigration visas, ensuring your business and personal goals move in perfect alignment. We bring deep expertise to the Brazil-Portugal-USA legal corridors and offer specialized drafting for Shareholders’ Agreements (SHA) and SAFE contracts that protect every stakeholder. Don't leave your international legacy to chance. Book a consultation with Pactum Global to structure your Portuguese holding company. Your journey toward a secure, global future starts with a single, strategic step.

Frequently Asked Questions

What is the minimum share capital for a holding company in Portugal?

The minimum share capital depends on the legal structure you choose for your entity. For a private limited company (Lda), the capital can be as low as €1 per share. If you opt for a public limited company (SA), the minimum requirement is €50,000. Most international founders prefer the Lda structure because it offers significant flexibility with a very low initial capital commitment.

Can a non-resident be the sole director of a Portuguese holding company?

Yes, a non-resident individual or entity can serve as the sole director of a Portuguese company. To do so, they must first obtain a Portuguese Tax Identification Number (NIF). While this is legally permitted, we recommend establishing local management or hiring employees to satisfy EU substance requirements. This proactive step ensures your company isn't classified as a "letterbox" entity during future tax audits.

How long does it take to get a NIF and open a company in Portugal remotely?

You can typically expect the entire process to take between one and three weeks. Obtaining a NIF for a non-resident usually takes just a few business days through a fiscal representative. Once the NIF is ready, setting up a holding company in Portugal can be handled remotely via a power of attorney. This allows you to complete the incorporation without traveling to the country immediately.

What is the difference between an SGPS and a standard Lda company?

An SGPS is a specialized legal form dedicated exclusively to managing shareholdings, which requires a mandatory statutory audit and strict regulatory compliance. A standard Lda is a flexible private limited company that can perform holding functions while also engaging in other commercial activities. In 2026, most investors choose the Lda structure because it provides the same tax benefits with far fewer administrative burdens.

Do I need a physical office in Portugal for my holding company to be tax-compliant?

Yes, maintaining a physical office is a critical requirement for demonstrating "adequate substance" under current EU directives. Your holding company can't simply be a mailing address; it must have a dedicated workspace where key management decisions occur. Demonstrating this local presence protects your right to access Portugal’s participation exemption and prevents other jurisdictions from challenging your company’s tax residency.

How does the participation exemption apply to capital gains on the sale of a subsidiary?

The participation exemption provides a 100% tax exemption on capital gains realized from the sale of shares in a subsidiary. To qualify, your Portuguese holding must own at least 10% of the subsidiary for a consecutive 12-month period. The subsidiary must also be subject to a corporate tax rate that is at least 60% of the Portuguese rate and cannot be located in a blacklisted tax haven.

Can a Portuguese holding company own assets in the USA or Brazil?

A Portuguese holding company can absolutely own and manage assets in both the USA and Brazil. Setting up a holding company in Portugal is an ideal strategy for investors operating in the Brazil-Portugal-USA corridor. Portugal’s extensive network of double taxation treaties ensures that income from these jurisdictions can flow through your structure with maximum efficiency and minimal tax leakage.

Is a statutory audit mandatory for all Portuguese holding companies in 2026?

Statutory audits are mandatory for all entities registered as an SGPS, regardless of their size or turnover. For standard Lda companies acting as holdings, an audit is only required if they meet specific size thresholds regarding their total assets, annual revenue, or number of employees. We help you monitor these compliance requirements to ensure your structure remains in good standing with Portuguese authorities.